In early August, Ethereum’s long-awaited London upgrade went into effect. It contained a package of Ethereum Improvement Proposals, or EIPs. The most consequential of these was EIP 1559, which changed the core fee logic. Prior to the change, Ethereum blockspace was auctioned off on a “first price” basis – effectively users would have to make […]

In early August, Ethereum’s long-awaited London upgrade went into effect. It contained a package of Ethereum Improvement Proposals, or EIPs. The most consequential of these was EIP 1559, which changed the core fee logic.

Prior to the change, Ethereum blockspace was auctioned off on a “first price” basis – effectively users would have to make educated guesses regarding the likely clearing price of blockspace. For the sake of guaranteed inclusion, they’d often end up overpaying. That was seen as inefficient.

CoinDesk columnist Nic Carter is partner at Castle Island Ventures, a public blockchain-focused venture fund based in Cambridge, Mass. He is also the co-founder of Coin Metrics, a blockchain analytics startup.

Thus, EIP 1559 was proposed: Every transaction in a block would pay the same price. The objective was to simplify fee logic, especially for blockchain developers, increase predictability and reduce the variance of gas prices.

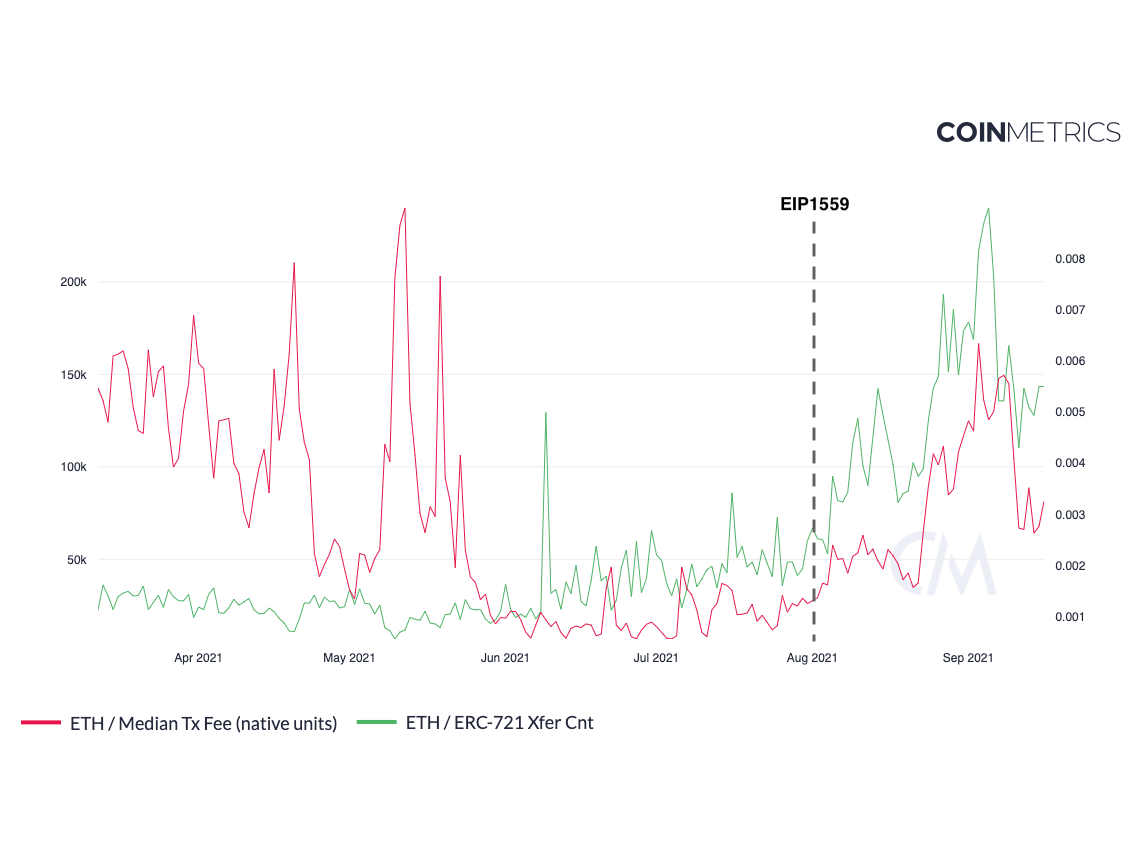

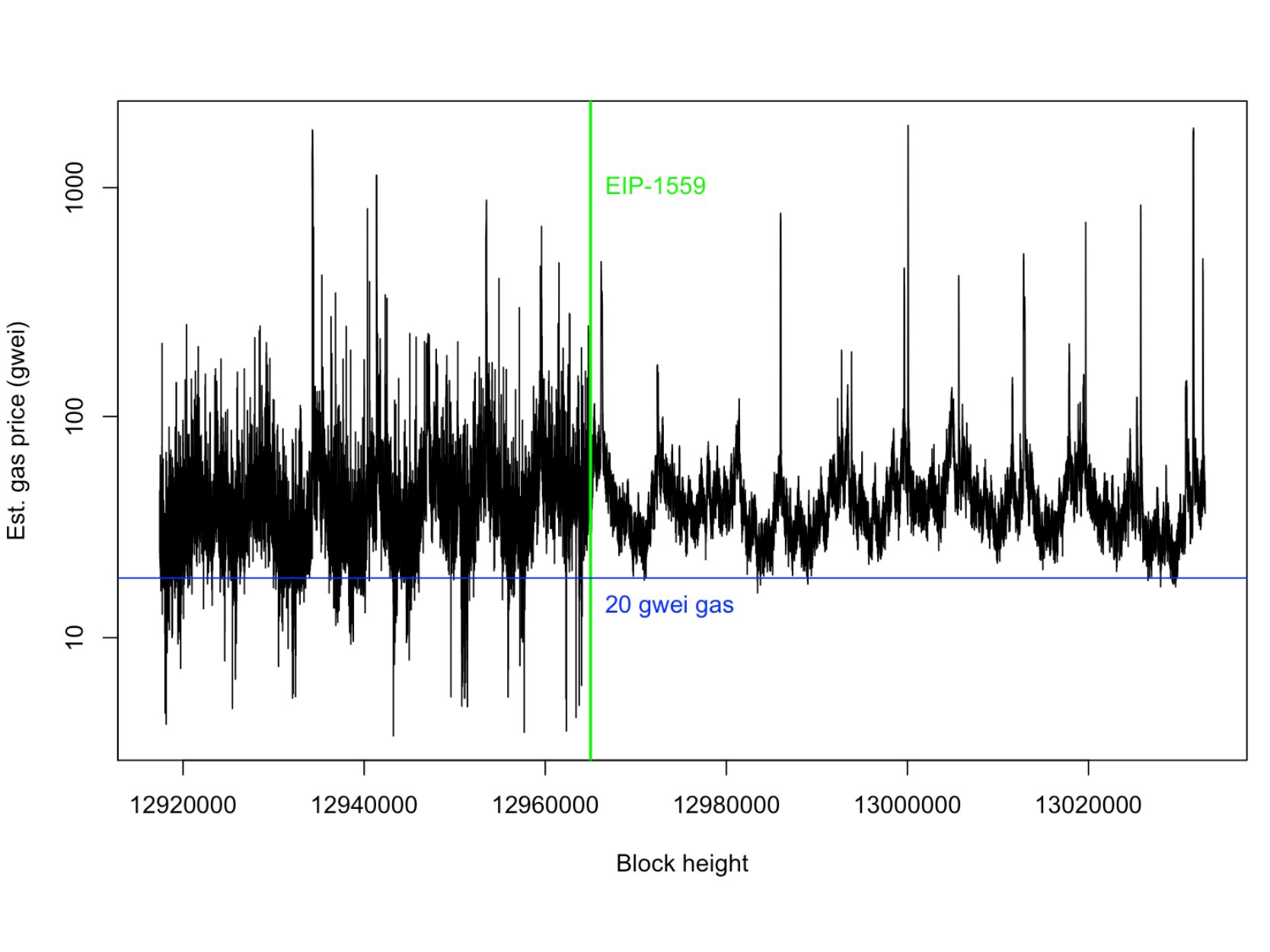

Based on the data we have so far, this looks like it has worked. Fees are indeed less volatile than they were before. They are, however, no cheaper, to the chagrin of some users. Ethereans close to the process insist that the tweak was never intended to cheapen blockspace. Insiders blame the surge in fees mostly on non-fungible token mania. Indeed, a cursory analysis lends some support to that theory.

The latest surge of NFT enthusiasm happened to coincide with the rollout of EIP 1559, so we won’t be able to tease apart the causality until this NFT episode subsides. Early analysis supports the idea that EIP 1559 has instituted a de facto near-term price floor on the price of gas, effectively eliminating periods of downtime (typically at night or on the weekends) when blockspace is cheaper.

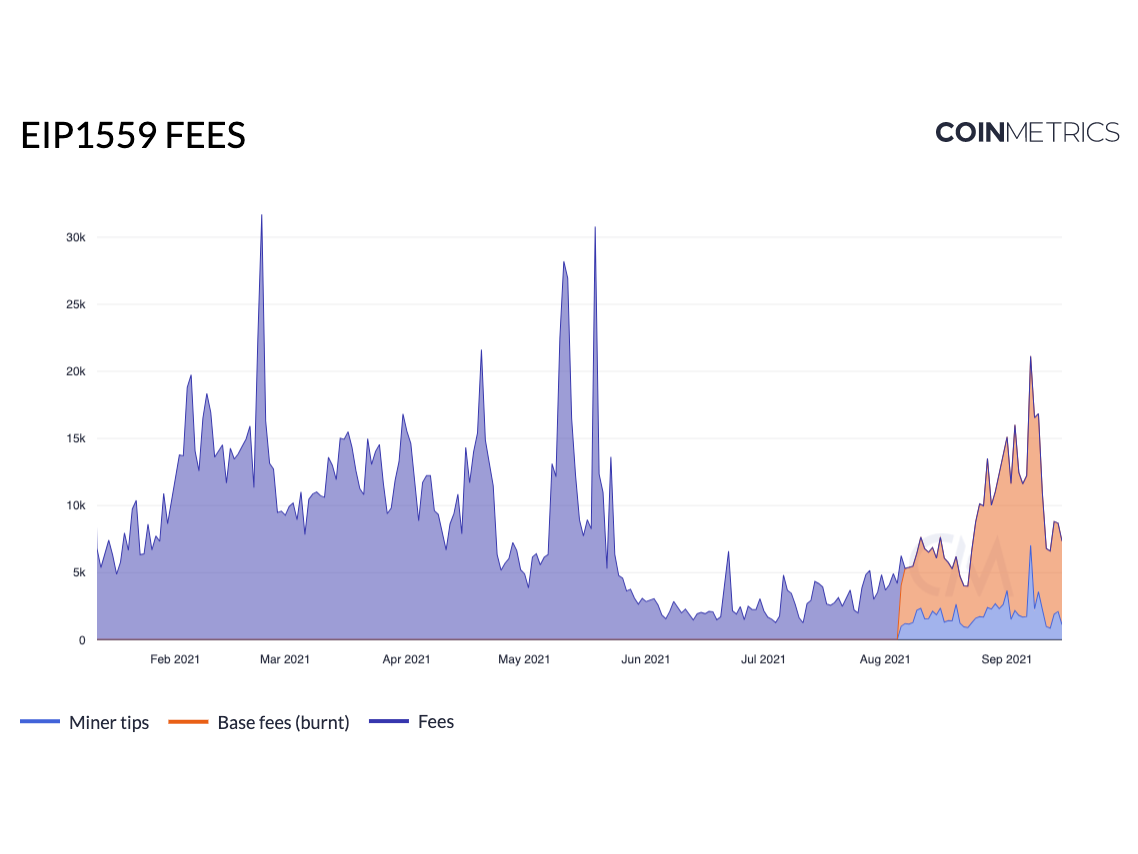

Based on a visualization of gas prices post EIP-1559 created by data scientist Takens Theorem, it looks like the change eliminated much of the downside volatility in gas prices but did not eliminate the right tail. Extreme fee spikes during periods of congestion still happen.

Removing the left tail of fees disempowered users who would set low “limit orders” on gas and were happy to wait for it to clear. Effectively, this change homogenized the way users had to bid on gas, pricing out those who were price sensitive and preferred to wait for low gas prices.

And then there’s the fee burning. The base fees are now burned, while miners collect some residual “tips.” This mechanic was included for a couple reasons: first of all, to privilege ether as the sole native currency of Ethereum, similar to the manner in which only USD can extinguish a tax liability in the U.S. Additionally, it eliminates the attack mode in which miners might stuff blocks with high fee transactions to bid up the clearing price of gas and force users to pay extortionate fees. This fee recycling attack doesn’t work when the base fees are burned.

But the fee burning design choice has economic consequences, too. For one, it disadvantages miners, stripping away a good chunk of the revenue they were previously earning. As a consequence of the change, only about a quarter of the fees users pay to access the blockchain today go to miners. Previously, they earned them all.

The remainder are burned, effectively constituting an ongoing “stock buyback” and retirement. This has amounted to more than 300,000 ETH burned in the 41 days since the change, representing a reduction of 2.3% of supply on an annualized basis. During days of high usage, the fee burn has fully sterilized the normal issuance associated with the protocol (in other words: the burn was sufficient to fully offset the new inflation).

If you look at the chart, it’s clear that miners have seen their fee revenue dramatically reduced, with the majority of fees being burned instead.

So the change has reallocated a continuous flow of economic rewards from miners (who eked out a living competing in the thin-margin game) to the existing holders of ether. By burning the fees, Ethereum has also decreased its expenditure on security. While Ethereum appears to be secure, reorganizations on smaller proof-of-work blockchains aren’t unheard of.

Ethereum is likely just fine at this level of security spending, but it’s not worth fully discounting the service that the miners perform. Their job is to create valid, linear blockspace with no forks. Decrease the wages paid to the mercenary army that defends your terrain, and it can more easily be paid off by an attacker. There’s a point where further decreasing miner revenue would put Ethereum at risk; granted, it’s probably at a much lower threshold.

The more serious problem with the fee logic change is that it pits token holders against blockspace consumers

Ethereum insiders are well aware of the effects of this policy on miners, and indeed disempowering miners has long been on the agenda. Miners don’t feature in the long-term plans for Vitalik & Co; in the fully proof-of-stake future that Ethereum is haltingly progressing toward, miners won’t have a role at all. Thus, their interests are not often considered when protocol changes are concerned; they are just near-term contractors and will eventually be discarded.

There’s a few problems with that. If you treat miners as expendable, they won’t maintain a duty of care toward the blockchain. For now, miners still occupy a privileged position in the transactional life cycle, as they control the ordering of transactions in a block. It’s well known that reordering (or selectively including or omitting) transactions offers economic rewards to the entities that control transaction selection.

Some miners have delayed taking advantage of this so-called “miner extractable value” (MEV) – which is hostile to end users – out of principle. Now that they are being squeezed out, they have no reason to seek to maximize the long-term value of the protocol. Indeed, especially as their fee revenue has been dramatically reduced, they are incentivized to seek revenue any way they can, even if it comes at the expense of users. Less direct protocol revenue could mean more MEV-based revenue and more exploitation of end users.

The more serious problem with the fee logic change is that it pits token holders against blockspace consumers. Holders now directly benefit from sustained high fees. The higher fees are, the more units of ether are retired. This is likely accretive to the unit price of ETH. However, it comes at the expense of actual users of the blockchain, who, ceteris paribus, prefer lower fees.

In a world where token holders are users (and vice versa), this isn’t a problem. But as Ethereum matures and seeks to attract mainstream corporate users who may seek to simply transact rather than hold, this apparently extractive relationship with transactors could well make it a tough sell. The analogy I’d draw here would be an electrical utility company raising prices for its consumers to buy back its shares.

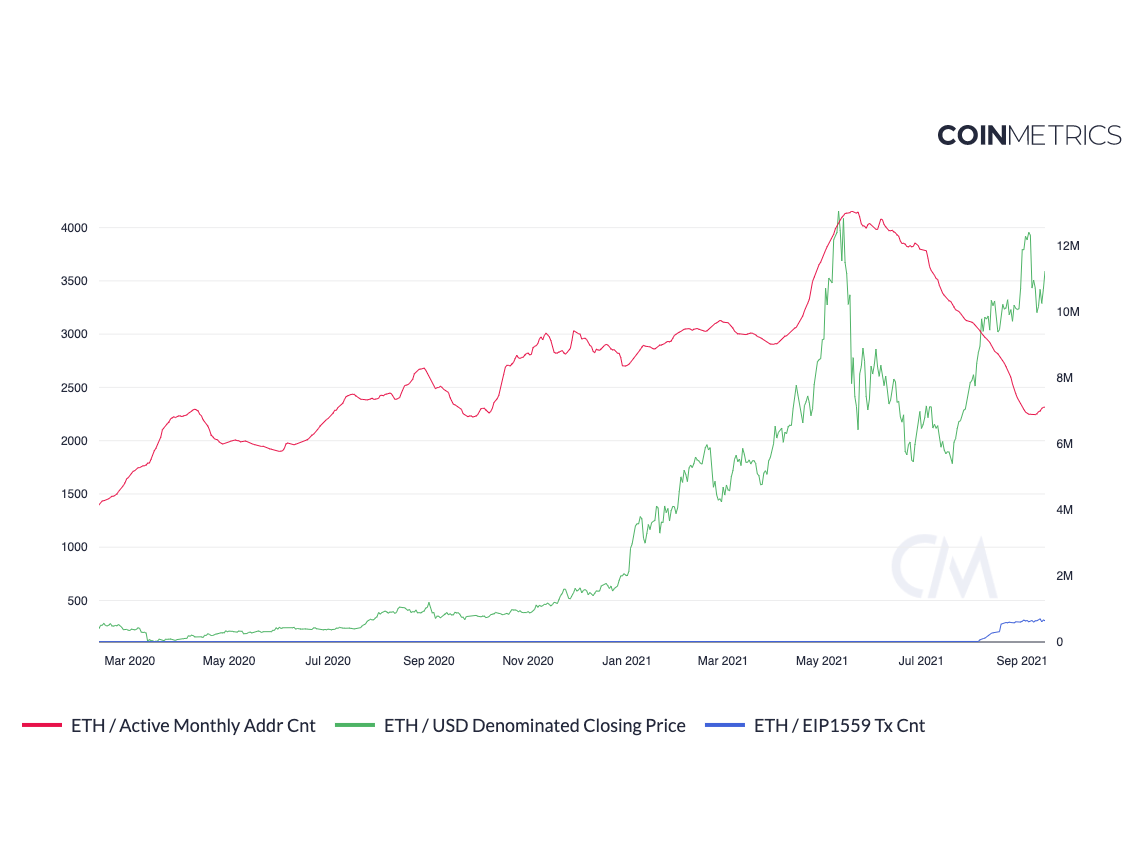

The best evidence that Ethereum has entered a new phase of life – from a scrappy upstart, to a mature protocol now extracting rents from consumers of blockspace – is a chart of monthly active users versus the unit price.

For virtually its entire history, the two variables have moved in tandem. That stands to reason: More usage meant more demand for ether itself. But, since July, the relationship has decoupled. Monthly actives have steadily declined, but ether has rallied strongly. Much of that rally is attributable to hype around EIP 1559 and the subsequent high rate of burnt fees. But one wonders how long the rally can last if the fee burning paired with high fees comes to antagonize large consumers of blockspace.

Even if EIP 1559 isn’t directly responsible for high fees, it’s hard to argue that the Ethereum insiders who make these decisions and own significant quantities of ETH are particularly upset about the fees, as they now financially benefit from the more deflationary environment that the change has brought about. If you are a large consumer of blockspace, you may bristle at the fact that your fees are not paying for security, but are instead being redirected to token holders.

This could come to a head in a future conflict over, say, block size. I can easily imagine a faction of transactors lobbying for a higher block size, in an attempt to create more blockspace and push down the clearing price of gas. But will large token holders, benefiting from the deflationary effect of the high fees, want to reduce the size of their user-financed stipend? The fact is that, due to the fee-burning mechanic, which has clearly been quite good for the price of ether, the individuals in control of Ethereum protocol design now have a meaningful incentive to keep fees permanently high.

The arbitrary change to the monetary policy is both short-termist and dangerous in terms of precedent-setting

The arbitrary change to the monetary policy is both short-termist and dangerous in terms of precedent-setting. It is short-termist in that it disempowers transactors, upon whom the entire investment case for ether is built. If you can’t attract firms and users to hold ether as working capital for transacting, that source of reservation demand will ebb away. Speculators are ultimately guessing that the protocol will see sustained future usage. The value of ether is at partly the discounted future expectations of token holders, contingent on future adoption. For those expectations to materialize, they will have to continue to persuade users that Ethereum is a stable and non-rent-seeking transactional venue.

It also sets a troubling precedent. Sure, the price rallied in anticipation of the change, and a good number of ETH have been burned, but the decision is no less arbitrary. Sound monetary policy is about setting monetary rules that cannot be interfered with – creating supra-human institutions that are indifferent to short-term political pressures. That was the objective of the gold standard, an institution that governed for hundreds of years.

Ethereum thus far hasn’t been able to commit to a stable monetary rule. If the issuance can be dialed down after a mere few months of discussion by insiders, the throttle can be opened up at a later date. Ethereum’s policymakers should consider committing to a rule that will guide policy for decades, not months. And given that this policy is redistributive, one wonders what protocol insiders will do next. Certainly, there is an unacknowledged political tinge to all of these decisions that are represented as merely engineering choices.

Against this backdrop, “Ethereum killers” have thrived. Alternative platforms like Algorand, Avalanche, Near and Solana promote themselves on the basis of low fees and fast transactions. Of course, they make (possibly unacceptable) decentralization tradeoffs to get there, and these blockchains are not without their own issues. But their case for an alternative is easier to make if the incumbent smart contract protocol is charging extremely high fees – $500 for a single Uniswap transfer is not uncommon – and arguably extracting rent in the process.

In an environment in which stablecoins are highly portable across chains and investors are eager to finance wallets, infrastructure and decentralized finance (DeFi) applications on novel blockchains, liquidity is less of a moat. It has never been easier for large consumers of blockspace to move their affairs to a new protocol. The fee pressure on Ethereum, which large token holders now perversely benefit from, could well push transactors to seek greener pastures elsewhere. Why choose to transact on a blockchain where you will inevitably face high fees – thus enriching insiders with the burn mechanic – when you could find another blockchain with cheap, or even subsidized blockspace?

EIP 1559 may well have been sound engineering in terms of meeting its core objective of reducing the variance in blockspace pricing. However, its largely unacknowledged externality – the redistribution of fees from miners to token holders – is troublesome. First, it’s an arbitrary decision made by a small number of insiders, and it affects the core economics of the protocol.

Second, it compromises the monetary credibility of the network and resets the monetary “Lindy clock” to 0. If issuance can be engineered downward, it can be raised later on. EIP 1559 also antagonizes miners, who still occupy an important position in the network and are now less disposed toward being fair stewards of the protocol. And lastly, it puts the interests of large token holders against those of current and future blockspace consumers. This could well harm Ethereum in the long run, if its alternatives are able to better align incentives and gain traction.